Navigating a Slow Market

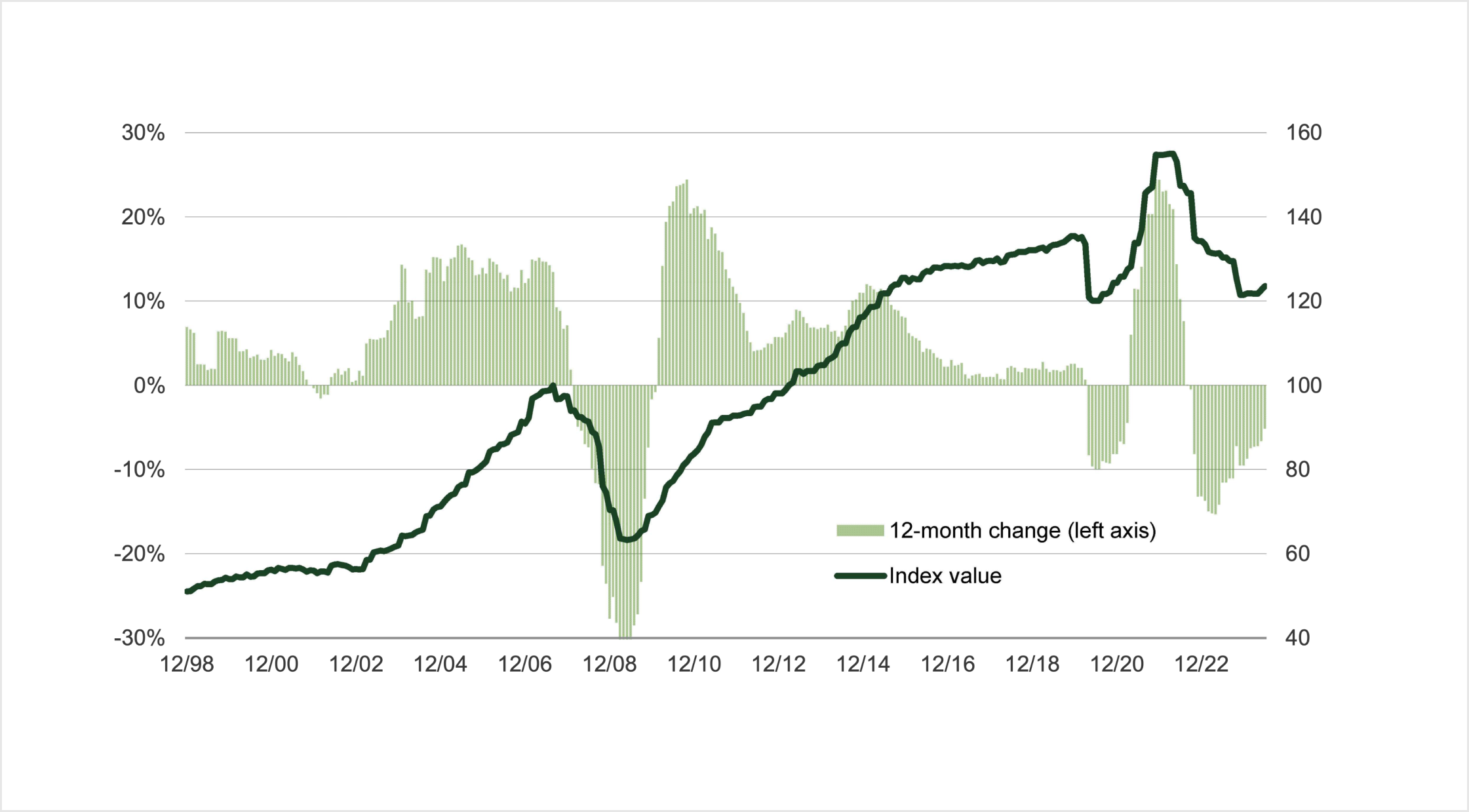

Over two years have passed since the Federal Reserve initiated its first interest rate hike, and it has been more than a year since rates have remained unchanged, at their highest level in 23 years.1 Now, the market is anticipating the advent of rate cuts, but the expectation is of fewer in number and slower in pace than widely believed at the start of the year.2 Although the timing and impact of such rate cuts remain unpredictable, this shift toward expecting rate cuts and the end of rate hikes has partially helped alleviate a nearly two-year-long market downturn.

.jpg)

From our vantage

point, the commercial

real estate (“CRE”)

market continues

normalizing and

adjusting to its new

reality. It’s not as if

interest rates are

excessively high from a

multi-decade

perspective; they’re

just excessively high

relative to twenty-four

months ago1 -

adaptation to such a

rapid

rate of change typically

takes time.

The word “scarcity” comes to mind when we consider today’s deal flow - transaction volume is down 60% since the initial rate hike in March 2022.3 However, the relative trickle of deals we do see is becoming more interesting to us, which leads us to believe we are in the middle of a market trough. Despite a marginally improved outlook for interest rates, we expect transaction volume to remain subdued in the short term. Consequently, we anticipate that deal volume on the Sammamish Realtor Marketplace will also remain relatively low in H2 2024 compared to our historical volume.

Overall, we are looking for opportunities to acquire properties adequately discounted from their peak values, preferably in locations where long-term market fundamentals remain intact, with an outlook that supports positive net absorption and strong population growth over the next five years, especially those with recovering urban centers. Some of these markets may be oversupplied in the short term. That may be acceptable, provided the pricing reflects the current environment. As for ground-up development, while not impossible, we observe it’s harder to scout these projects today due to a combination of generally expensive debt, scarcity of lenders willing to lend, expanding cap rate environment, and tepid overall rent growth.4

To keep you updated, we will closely monitor interest rates, inflation, and other economic indicators as economic trends evolve. Our H2 2024 report incorporates our industry knowledge and thorough research to construct our outlook and strategies across various CRE asset classes.

-1.jpg)